Right of First Offer in Commercial Property: How to Protect and Leverage Your Position

Article Summary

- A watertight ROFO clause needs four things: a clear trigger, notice requirements, a response window, and disclosure obligations. Vague drafting on any one is where disputes begin.

- A ROFO gives you the first move; a ROFR gives you the right to match after the seller has tested the market. Which you hold determines your level of control.

- Price constraint thresholds protect rights holders from being undercut by marginally higher third-party offers.

What Is Right of First Offer?

A right of first offer (ROFO) is a negotiated clause that gives the holder the right to make an offer on a property before the landlord markets it to third parties and sets out exactly what happens if they try to circumvent it.

In a commercial lease context, a right of first offer gives a tenant the first opportunity to make an offer on a space before the landlord markets it to third parties.

Whether it's an adjoining unit going up for lease or the landlord decides to sell the entire building, you as the ROFO holder get first access to make an offer, but the right is only as strong as the language behind it.

A well-structured ROFO clause clearly defines four components:

- The trigger: What activates the right. A decision to sell? A decision to lease adjacent space?

- Notice requirements: How and when the landlord must inform you, including the method of delivery and what information the landlord must include in the notice.

- The response window: The exact timeframe you have to submit an offer once notified.

- Information disclosure obligations: What the landlord must provide to enable proper due diligence, including rental terms, asking price, and any known material defects.

Portfolio sale carve-outs are a common exclusion in ROFO agreements. Without clear limits, they can effectively hollow out your right.

What Is the Difference Between ROFO and ROFR?

ROFO requires you to act before the seller tests the market. ROFR lets you respond after they have.

A right of first offer is triggered before a property goes to market. The owner must come to you first, you make your offer, and then they decide whether to accept or move on to third parties.

With a right of first refusal (ROFR), the owner markets the property freely, receives a third-party offer, and only then must give you the chance to match it.

| ROFO | ROFR | |

|---|---|---|

| When it triggers | Before the property is marketed | After a third-party offer is received |

| Who sets the price | The rights holder | The third-party buyer |

| Seller flexibility | High | Lower |

| Buyer protection | Moderate | Strong |

| Impact on third-party interest | Minimal | Can deter competing bids |

| Best market conditions | High demand, low supply | Slow or uncertain markets |

In a high-demand market, a ROFO is extremely valuable. Off-market access before competing bids emerge can be the difference between securing an asset and losing it.

In a slower market, a ROFR carries more weight because you can let the owner test the market before deciding to act. Understanding types of property ownership in the UK is useful context, as ownership structure affects how these rights are registered and enforced.

When selling commercial property, owners with ROFO obligations must factor the notification process into their timeline from day one.

How Much Time Do You Have to Act on a Right of First Offer?

Response windows are shorter than most investors expect, and your financing needs to be ready before the clock starts.

A ROFO notice is not an invitation to begin your research. By the time a landlord or seller triggers the clause, you should already have a clear view of the asset's value, your financing position, and your appetite to proceed. Response periods in UK commercial property typically fall between 30 and 60 days from formal notification, though the exact window will depend on what is outlined in the ROFO clause. The notice period is time to execute, not evaluate.

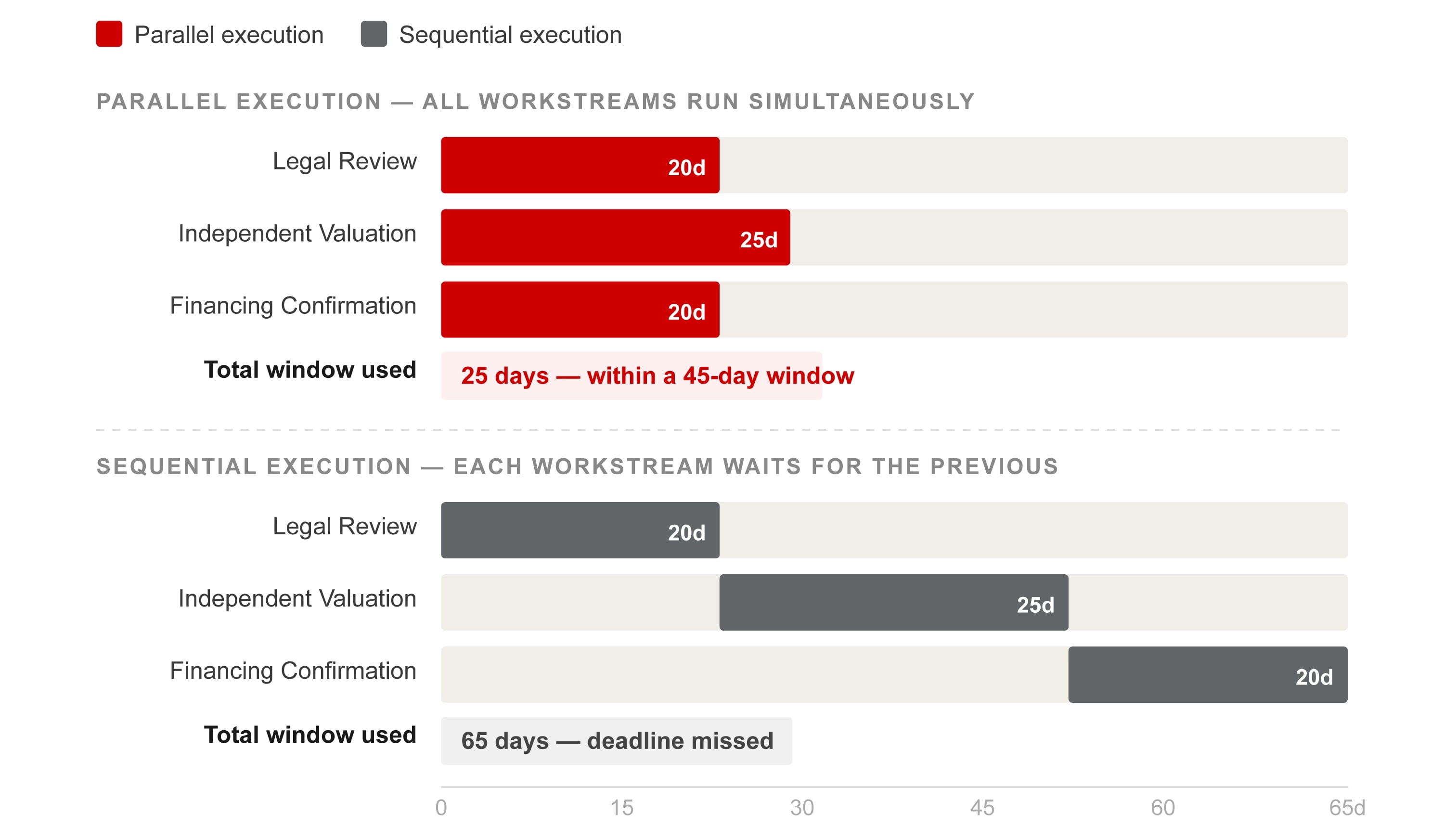

A well-used response window covers three things in parallel: legal review of the title and lease structure, independent valuation, and confirmation of financing. Running these sequentially rather than simultaneously is where investors lose time and miss deadlines. The advantages of using a commercial agent are particularly clear in time-pressured scenarios like these. When buying commercial property, experienced investors maintain relationships with valuers and solicitors who can mobilise quickly.

Financing is where most ROFO exercises fall apart.

Before a ROFO is triggered, make sure you have:

- A conditional credit facility you can activate quickly.

- A pre-run discounted cash flow model assessing the asset at various price points.

- A firm grasp on how to calculate the net present value of the opportunity relative to your cost of capital.

Keeping these in place is not a one-time exercise. A conditional credit facility should be reviewed annually or whenever your capital structure changes materially. Your DCF model should be refreshed if the asset's occupancy, lease terms, or comparable evidence shifts. The signal to update is not the ROFO notice itself but any material change in the asset or your own financing position.

The difference between the two approaches is not marginal:

Parallel vs Sequential Execution: Why Timing Your ROFO Response Matters

In a typical ROFO response window, running legal review, valuation, and financing in parallel keeps execution within the agreed timeframe. Sequential execution can double that window, often causing investors to miss their deadline entirely. The days shown represent an illustrative 45-day example.

How Do Price Constraints Protect ROFO Rights Holders?

A minimum price threshold prevents sellers from accepting marginally higher third-party offers without first returning to you.

Price constraints set a threshold below which the seller cannot accept a third-party offer without returning to you first. The exact threshold depends on what was agreed when drafting the clause, but the principle is consistent.

If your ROFO agreement includes a 5% threshold and you offered £1 million, the seller could not accept a third-party offer below £1.05 million without giving you another opportunity to purchase.

Price constraints only work if your original offer is grounded in a credible valuation. An offer that is too low gives the seller an easy reason to reject it and go to market.

For income-producing assets, anchor your valuation to commercial property yields and cross-reference against net initial yield (NIY) benchmarks for comparable assets in the same submarket.

Commercial Properties For Sale

In illiquid markets where comparable data is scarce, consider including an independent commercial building valuation clause that requires both parties to accept a RICS-assessed value as the baseline if they cannot agree.

For industrial assets specifically, a live look at industrial property for sale sharpens your read on comparable stock and asking prices before you submit a ROFO offer.

What Happens to Your ROFO Rights If a Property Owner Enters Insolvency?

A ROFO clause does not automatically survive insolvency proceedings, and unprepared rights holders often find out too late.

When a commercial property owner enters administration, control passes to the appointed administrator, whose role is to act in the interests of creditors rather than the property owner.

An unregistered ROFO is a contractual right between two parties. If an administrator sells the property to a third party, that buyer may take the asset free of your right entirely. Taking legal advice on how to protect your ROFO on the title register at the point of negotiation is a step many rights holders overlook until it is too late.

How Do You Negotiate a Stronger Right of First Offer?

The best time to strengthen a ROFO is before you sign, not after you receive the notice.

Market conditions dictate your starting position. In a market where quality stock is scarce, you will have less leverage to demand robust ROFO terms. Where vacancy rates are elevated and landlords need to retain good occupiers, your negotiating position is stronger. Timing your ROFO negotiation to coincide with that dynamic is itself a strategic decision.

In markets where landlords are motivated to retain strong occupiers, hybrid structures can be achievable. A ROFO on the initial sale combined with a ROFR on any subsequent resale within five years gives meaningful protection across two transaction cycles, though landlords will typically resist this combination unless vacancy pressure gives you genuine leverage.

In particular for retail assets, understanding your retail space requirements and long-term expansion plans before entering negotiations ensures your ROFO genuinely serves your investment strategy. Considering the right retail space to let gives you a chance to find assets with expansion potential that make it worth pursuing a ROFO when you sign.

Frequently Asked Questions

Can a ROFO be transferred or assigned to another party?

Generally, no. Most ROFO agreements include exclusivity clauses preventing the rights holder from transferring the right without the owner's consent. If you anticipate a future company restructure or transfer to an affiliated entity, include explicit assignment provisions at the drafting stage.

What happens to a ROFO if a sale falls through after the right has been triggered?

This depends entirely on the reinstatement language in your agreement. In well-drafted clauses, the ROFO resets automatically if no third-party sale completes within a defined period.

Does a ROFO work differently on a leasehold asset versus a freehold?

Yes. The value of a leasehold ROFO is directly tied to the unexpired term of the lease at the point it is triggered. A freehold ROFO should be registered at HM Land Registry as a notice or restriction on the title, as an unregistered right may not survive a sale to a third party.

How does a ROFO affect a property's value in the eyes of a lender?

Lenders are cautious about perpetual ROFO rights with no sunset clause, as these can reduce perceived marketability and affect loan-to-value calculations. Structuring the ROFO with a defined term and an option to renew by mutual agreement addresses most lender concerns.